Power laws rule everything around us. This is a core principal of what we have largely come to learn in a world dominated by this narrative, which has also helped proliferate the concept of Asymmetric Upside.

Within traditional tech/Web2, due to the compounding nature of moats (most notably network effects) and duopolistic markets, it is often assumed that outcomes follow a colloquial power law distribution in which the top ~5-10% of outcomes will outweigh the value created by the next ~90% of outcomes.1Please spare me the “actually it’s 80/20” comments, as in modern portfolio dynamics it skews even harder than this distribution.

Tech companies have historically accumulated value at an astounding rate and scale, one that has surprised even the brightest tech investors over the past 5-7 years. This is due to both the structural advantages that (often) closed-source, walled garden, platform companies that continue to accumulate horizontal scale are able to benefit from, in addition to the financing dynamics within tech leading to fairly binary outcomes as public markets have often been reserved for a certain scale and risk level of companies.2This was perhaps broken in 2020/2021 with the SPAC craze, of which most of these companies have puked up returns, are facing lawsuits, and likely will be taken private, acquired, or obliterated over the next few years.

The Fat Protocol thesis was a good framework to understand value accrual in the early days of crypto and has proven to be very true, with layer 1 protocols accumulating much of the value. However as crypto as an industry matures and tokenization has been adopted as the dominant value capture and marketing tool, it is my belief that we could see this power law dynamic, a dynamic which serves institutional investors largely, begin to be less true.

Put more specifically, the value accrual of crypto protocols today and tomorrow may follow more of a normal distribution than power law distribution. There are a few reasons:

- The open-source nature of crypto means that forking and vampire attacks can occur once a certain level of product-market fit is achieved. This allows for incremental iteration to capture meaningful value via a fork, effectively spitting in the face of the Web2 mindset that 10x or 100x products are needed to win.

- The fast value accrual creates incentives that often don’t lead to sustainable moats being created within crypto protocols. In DeFi Summer we saw large amounts of wealth generated via yield farming and a larger bull run in crypto token prices. This paired with general unsophistication of how we analyze revenue or business durability, and thus metrics, caused DeFi protocols to trade at insane multiples in reality, along with ponzi dynamics that caused large scale buying. In Crypto, due to the lack of aforementioned mid to long-term moats, founders and communities must continue to evolve their product due to lack of compounding of existing success and network effects (again, due to point #1). Put more bluntly, once a core team has amassed millions to billions in wealth and the token has been farmed and dumped, it’s hard for projects to have incentives to work through a second bear cycle or downturn and break the next step function of network value.

- Tokens as arenas for PVP trading. There are a number of tokens today that carry network values of $50-$500M with decent liquidity depth that effectively act as playgrounds for traders, almost regardless of the underlying asset. This dynamic allows investors at moderate scale to exit their position either slowly or in tranches despite very little network activity or usage of the underlying protocol. In Web2 these companies just die due to inability to raise new venture financing, in crypto they exist as zombies on your CEX of choice in perpetuity.

- Related to the last point on #3, the universe of buyers for these assets is massively larger than private technology companies. This creates price discovery in both directions that private markets don’t have.

To put some admittedly shoddy data around this, I quickly pulled all tokens from CoinGecko, removed L1s, L2/sidechains, Meme, and low trading volume tokens in order to see how distributions of outcomes would look.3I promise you I missed tokens and one could argue semantics around a variety of tokens I’m sure I did this specifically as IMO L1s would skew all data that is meant to be forward looking and largely do follow a power law and will for some time, and meme tokens shouldn’t be invested in on the institutional side.

The above chart is a distribution of crypto market caps from ~$11B to $20M. What we see in terms of distribution of returns is as follows (again these are not at all exhaustive and this data is very imperfect and likely undershoot altchain MCs by a fair amount):

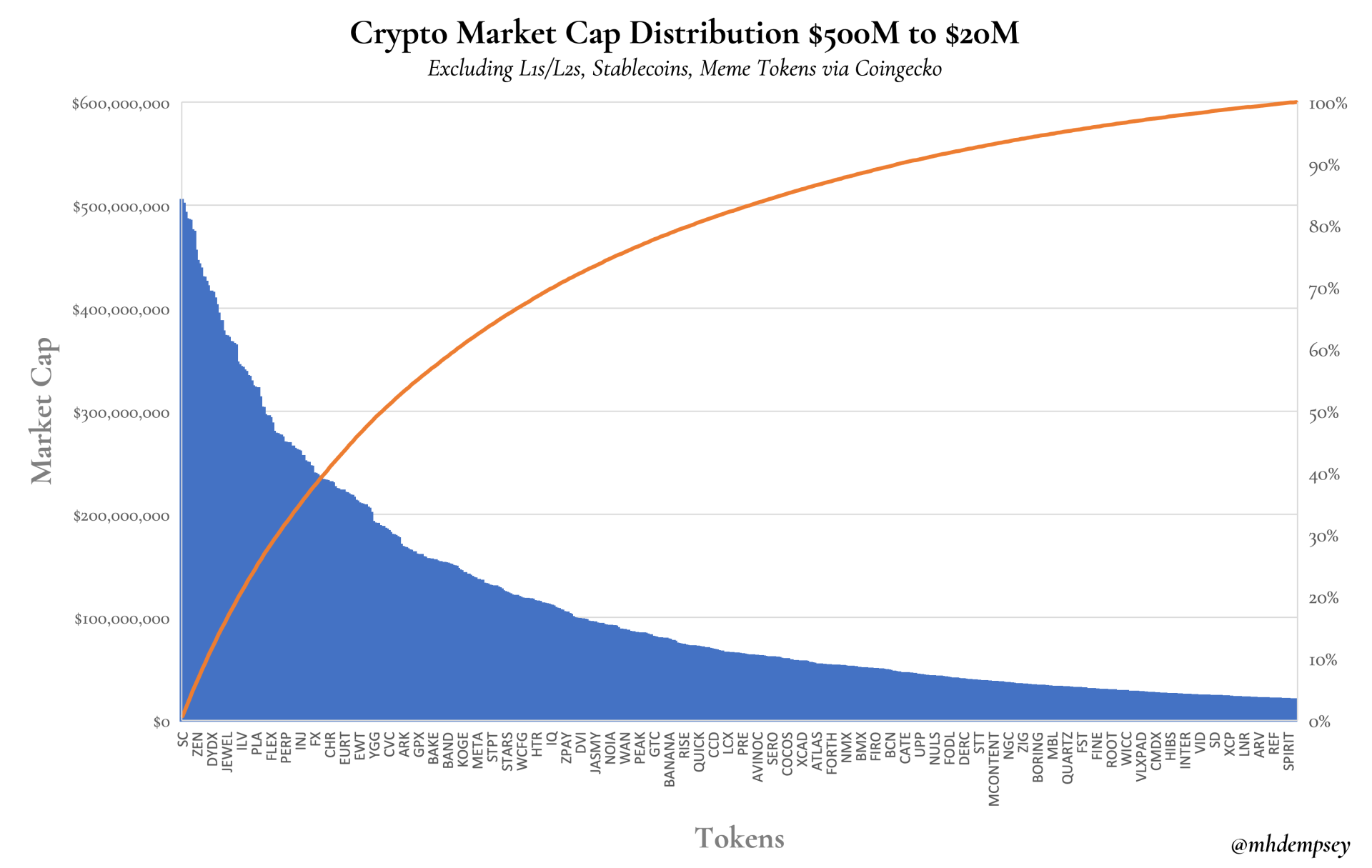

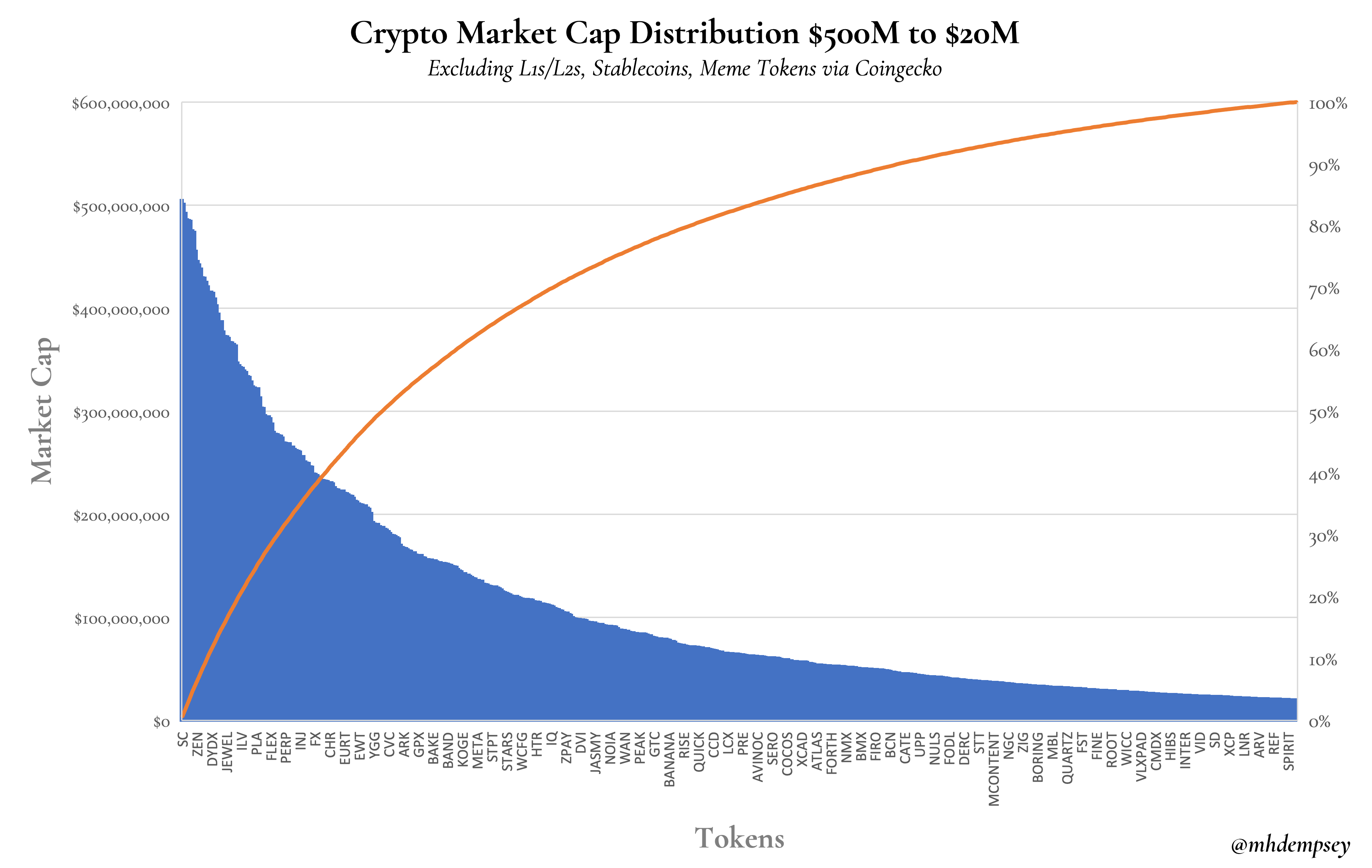

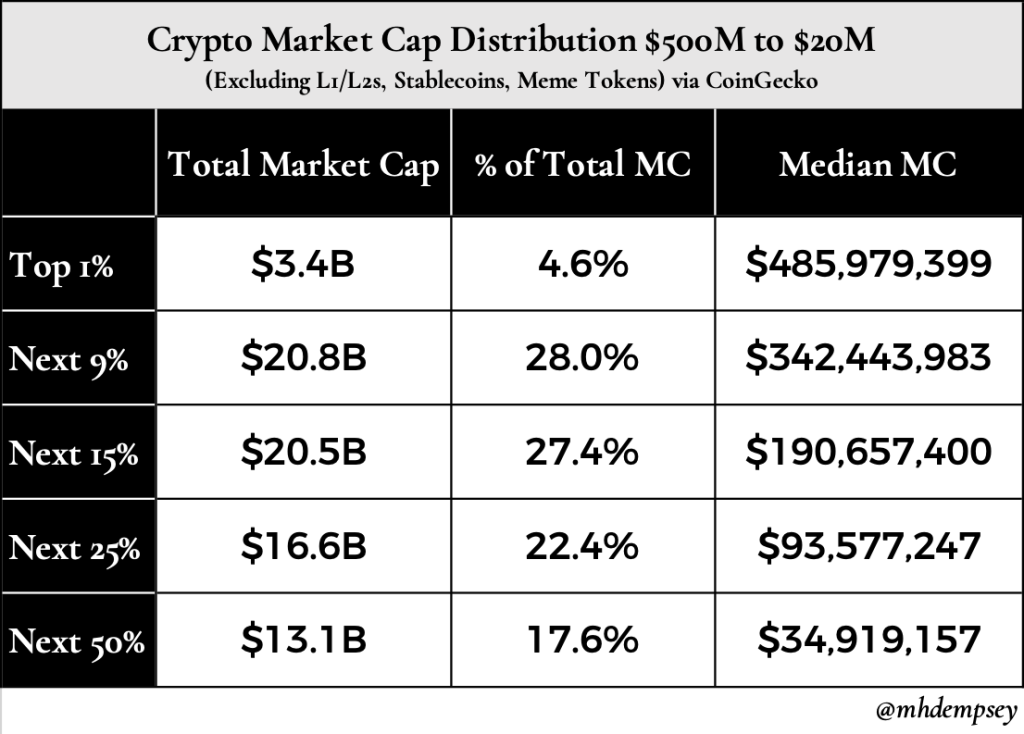

We see a strong distribution of returns with almost half of all tokens in our cohort showing a market cap north of $100M. This next chart is more interesting and speaks a bit more to normal distribution dynamics within crypto, looking at market caps for tokens $500M to $20M:

When we peel back the data a bit more to a granular level, what we see is a distribution of outcomes where in this lower tier of market caps, the top 25% of tokens in this cohort are above $140M in market cap with strong median outcomes in each percentile.

So, what does this all mean? The jaded take is that it means nothing. There are a huge % of projects that never launch a token, and as crypto continues to mature it is likely loss ratios will continue to expand due to the number of new projects launching.

However I believe this information deserves to be looked at.

What led me down this journey initially was a core belief that due to a variety of factors listed above, return distributions for a wide number of investors with a certain level of access and picking ability could look slightly less power law driven than in Web2. This has implications including fund sizing and outcome distribution for institutional investors, perhaps loss ratios for all investors, as well as valuation decisions for founders (and investors) as they model returns.

This is especially important when we consider liquidity, vesting schedules, and token unlock dynamics for teams as well as investors. In Web2 we have seen a trend where founders are taking liquidity earlier and earlier as prices raise. This dynamic doesn’t really impact prices or the companies themselves.

In Crypto what we historically have seen has been an entire class of the token supply having liquidity that often creates immense sell pressure on a token and pushes token price down further and further over time, perhaps leading to irrecoverable sentiment for the token and life changing outcomes for the early team and investors.

In almost all of these cases I believe the solve for this is to push for this longer-term value accrual or to be very clear about the type of project being built. Not all projects, just like not all companies, need to be aiming for massive scale, multi-billion dollar outcomes versus building a core piece of infrastructure or a public good that creates value for early believers at a smaller scale.

In the cases that the team and community do want to aim for the type of scale we’ve seen historically in venture markets, the answers are once again to be very intentional about liquidity 4(I’ve been vocal about how illiquidity is a very underexplored vector of competition and value accrual in crypto), vesting, and evolving tokenomics over time. In addition, these dynamics are why community engagement and storytelling + narrative building within the broader ecosystem are the most powerful levers to pull in order to both sustain downturns, incentivize early value capturers to stay on for the long-term without using aggressive liquidity mining, and give your project leeway with its community to experiment with novel mechanisms related to token value appreciation.

None of the data presented above is conclusive and there are likely things others will be able to glean from it that I haven’t laid out in this post. With that said, as we enter another wave of maturation and institutionalization of Crypto as an asset class, I believe it is important to understand how distribution of outcomes changes over time and thus, what decisions should builders, communities, and investors make along the way.

Recent Comments