Disclaimer: I believe that unless you are one of a few firms, there is no possible claim that there is a “correct” way to do venture, only to treat people with respect along the way.

Venture capital started as a network heavy business and arguably still is to many. I don’t think that is dominant anymore.

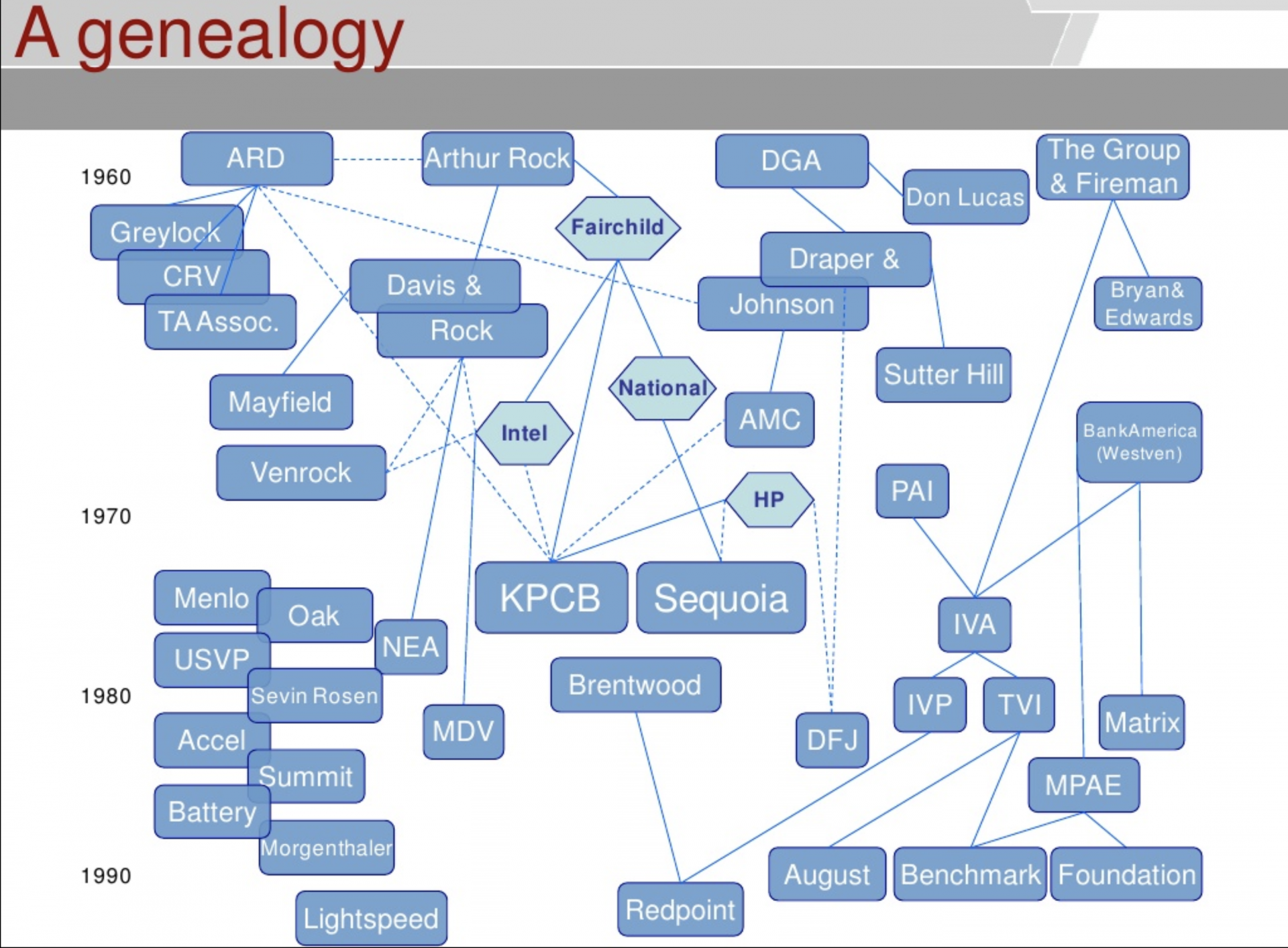

The Early Days: VC was the ultimate network business

Venture capital started as the ultimate network business, with a tight-knit web of humans for decades. It looked like this:

After the web 1.0 bubble, there was not an abundance of capital, and thus power swung back towards VCs as the market cooled. Those VCs, based on 2008 data, were an average age of 46, 79% were men, 87% were white, and 53% had MBAs (of which 60% went to Harvard or Stanford). Based on demographics like that, it’d be pretty difficult to not be a tight-knit, network-driven industry.

Then, 2-7 years before the 2012 Facebook IPO, came the first wave of elite seed firms like Baseline, First Round Capital, Floodgate, Foundry Group, SV Angel, True Ventures, SoftTech, and others.

As company formation costs fell due to a variety of technological drivers, paired with startups being “hot” again, we saw institutional capital want more exposure to private market technology risk. Partners spun out, founders started funds, and angels institutionalized.

The Birth of Seed & Verticalized Funds

“In angel investing, you don’t really have competitors. You go ahead and do your thing…I don’t look at Internet or Internet investing as competitive, generally.” — Ken Lerer, 2010

We all know this trend accelerated, with some seed funds graduating to series A+ firms, and quickly everyone (especially non-GPs who were stuck underneath partners unwilling to give up meaningful carry) wanted their own seed fund. The issue was, LPs had been hit up with the seed pitch now for the past 5+ years. And in the same time period, re-ups had come more and more often as fund deployment periods went from 5 years to 3 years.

These newer seed firms needed to differentiate as the “seed” story was played out.

This led to a wave of vertical-centric seed firms. Lemnos (2012 incubation fund I) and Root Ventures (2015 Fund 1) became known for hardware, Forerunner (2012 fund I) became known for consumer, Lerer Hippeau become known for NYC/Web (2010 Fund 1) and on and on it went.

The Venture Capital Explosion

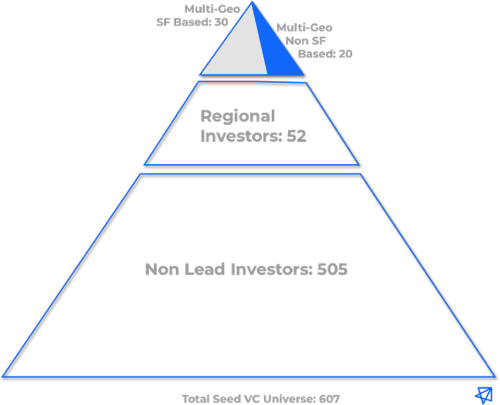

Between 2003 to 2010, an average of 58 seed funds were raised each year but in the past 7 years, that average spiked to 137 (or a 2.3x increase). – Eric Feng,

And now it’s 2019. The deployment periods for some funds have collapsed to as short as 18 months, there is a seed fund for everything, and series A+ firms have grown into full-stack financing machines with $1B+ funds designed to take companies from A to IPO, and many with scout programs to build the top of the funnel.

This hyper-crowded market has swung the pendulum back to old times, with LPs being sold either more explicit networks, or similar economics as the 70s.

The former manifests itself as unicorn-mafia funds (ex-uber employee fund, ex-airbnb employee fund, etc.) built around the idea that people want to raise money from their ex-coworkers and/or access will be materially better because of this relationship. The latter manifests itself as startup studios that have outsized ownership economics.

So we’ve got a ton of seed funds, plenty of post-seed capital, and some moderate differentiation. We also have a 7x increase in $1B+ outcomes from a decade ago.

But when I look around at seed stage venture, where the universe of companies is truly unknown, I still believe firms are relying on serendipity. And there are many firms that are trying to engineer serendipity at a high rate by sending analysts (and the partners themselves) to events 3–4x/week, actively trying to setup deal flow catch up calls, or aggressively stalking demo day lists, all born out of the fear that they will miss the next Stripe/Uber/etc.

And how do they scale up these teams to chase these competitive deals in an ever-expanding seed stage funnel? They raise more money.

As their seed fund gets bigger, they now need to write a $1.5-$2M check to get the proper ownership to 3–4x their $100M+ seed fund. At the same time it’s become more likely that interesting deals don’t get sent to them because…well the math doesn’t work for other investors to hit their ownership targets.

Or as Rob Go astutely points out, “firms that have built their models around aggressive deal trading will struggle.”

Now we have:

1) Larger seed funds, that are hyper-competitive (and often generalists due to fund size and scope creep).

2) Which means that seed funds need to tell founders that it is best for their business to only have them and no other meaningful checks in the round, so they can write $1.5M+ and get ~15%-20% ownership.

3) But unless you’re a top tier firm, your capital could be viewed as a commodity, and thus it’s clearly not dominant for a generalist firm to be the only investor (which is ok because…we’re humans, and we can’t be everything for everyone), and thus you are at massive risk of being pushed down in ownership and allocation.

4) And then in order to make the math work you’re reliant on multiple $1B+ outcomes, despite a large % of VC-backed M&A transactions happening below $300M.

5) So we now have some seed VCs telling investors that they will be able to increase ownership from seed to A/B or at worse do full pro-rata to maintain. The problem is that in reality, pro rata allocations from Series A+ remain increasingly difficult to maintain, as those $1B+ funds, that have infrastructure (and fees) to in theory actually be everything for everyone, need to put more money to work in their rounds. So you don’t get to defend ownership nearly as efficiently as even 5 years ago. And often any pre-empted offer for a pre-series A round could just turn into a pre-empted full series A process.

All of these things boil down to the core truth that most Seed stage firms today have to be small (either ridealong checks or non-hyper competitive leads), early, and/or different enough to be one top-priority thing for a subset of founders.

I recognize that I just doomsday scenario’d a bunch of components of seed stage venture capital, so I figured it’d only be fair for me to share my own (highly biased) view on what does work at some >1 firm scale at the seed stage.

First, forward looking macro-factors that I strongly believe in:

- VC returns have been persistent, but with each new innovation cycle turn (infrastructure to personal computing to web to mobile and onward) new successful VCs have been birthed that have become part of the persistence. The power law of venture will remain, but will be slightly more distributed.

- Private markets are going to continue to capture the returns in many sectors, and thus it will be attractive for LPs to be invested in a larger subset of tier 1, tier 2, and maybe even tier 3 VC firms from a returns perspective. This will be even more evident as we potentially enter tumultuous public market performance that shows lower yield over the next decade than the prior decade+ bull-run we’ve had.

- The compounding effects of venture as an industry are unique vs. any other industry. Brand flywheels are strong absent of results due to opacity of quantitative measures (i.e. we both bury the dead slowly and quietly on failed startups, and cheer the good loudly on less-than-incredible fund exits/performance).

- Brand signaling can create unfair advantages. I.e. If Sequoia invests in a company, statistically that company is more likely to raise money than if another investor does. Building a lasting brand matters.

More specifically the seed fund strategy that I believe in:

- Keep fund size small — Leading a round today is rarer than we think, and just means conviction and ability to put down a term sheet (and large check), but not necessarily 60%+ of the round. There has never been more follow-along capital at the seed stage and rallying investors around your conviction and lead check is a powerful thing that solves for some disadvantages of smaller funds.

- Remove noise and keep focused — Small fund size enables myself (and other similar funds) to not care about missing the next billion-dollar marketplace business. The funnel has widened (as seen above) , and only looking at a piece of the funnel is scalable/realistic. Yes, hit rate needs to be better, but I’d argue that while it’s gotten statistically harder to identify a fund returning company, it’s become exponentially harder to win meaningful allocation in that deal.

- Build an informed view of the world – This allows investors to compete on the axis of both having a deeper understanding of a space versus the average investor, theoretically have an ability to know what they are looking for at a faster pace (and thus move faster), find/track things earlier due to focus, and meaningfully compete via outbound deal flow by using ammunition that they’ve built up in research.

These last two points specifically are the only way in which I feel I am able to advantageously do venture. However, as I said before, it’s not immediately clear to me that one strategy in seed stage venture is dominant.

Small funds have dominant return profiles for today’s fundraising dynamics, high velocity funds have dominant statistics for today’s outcome distributions, full-stack funds have dominant funnel building for today’s growing prices, and concentrated funds have dominant return distributions if you can pick.

What is clear to me is that venture is changing rapidly and if you aren’t thinking about these things in real-time, you’re not doing your job.

Recent Comments